BTC ETF Proxy: IBIT / BITI Paper Strategy

Review package for the low-frequency BTC/ETH residual signal executed with US-listed BTC ETFs. The paper deployment is long-only at the instrument level: long IBIT, long BITI, or cash.

Launched Conservative Variant

Sharpe

1.90

US-session conservative lag

Total Return

318%

2024-05-08 to 2026-05-11

Max Drawdown

-22.65%

Backtest drawdown

Trades / Year

51.3

Low-frequency daily signal

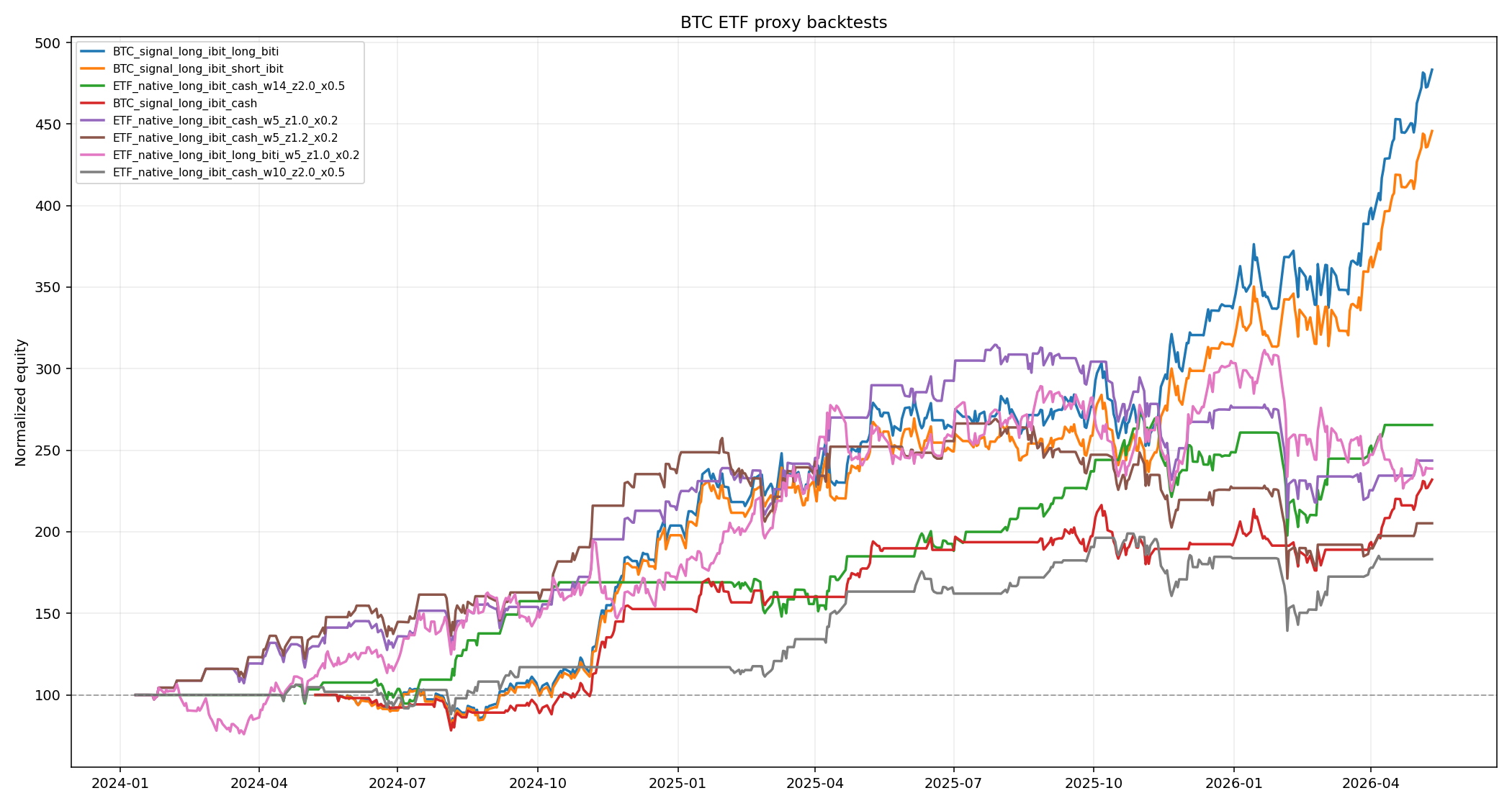

PnL Curves

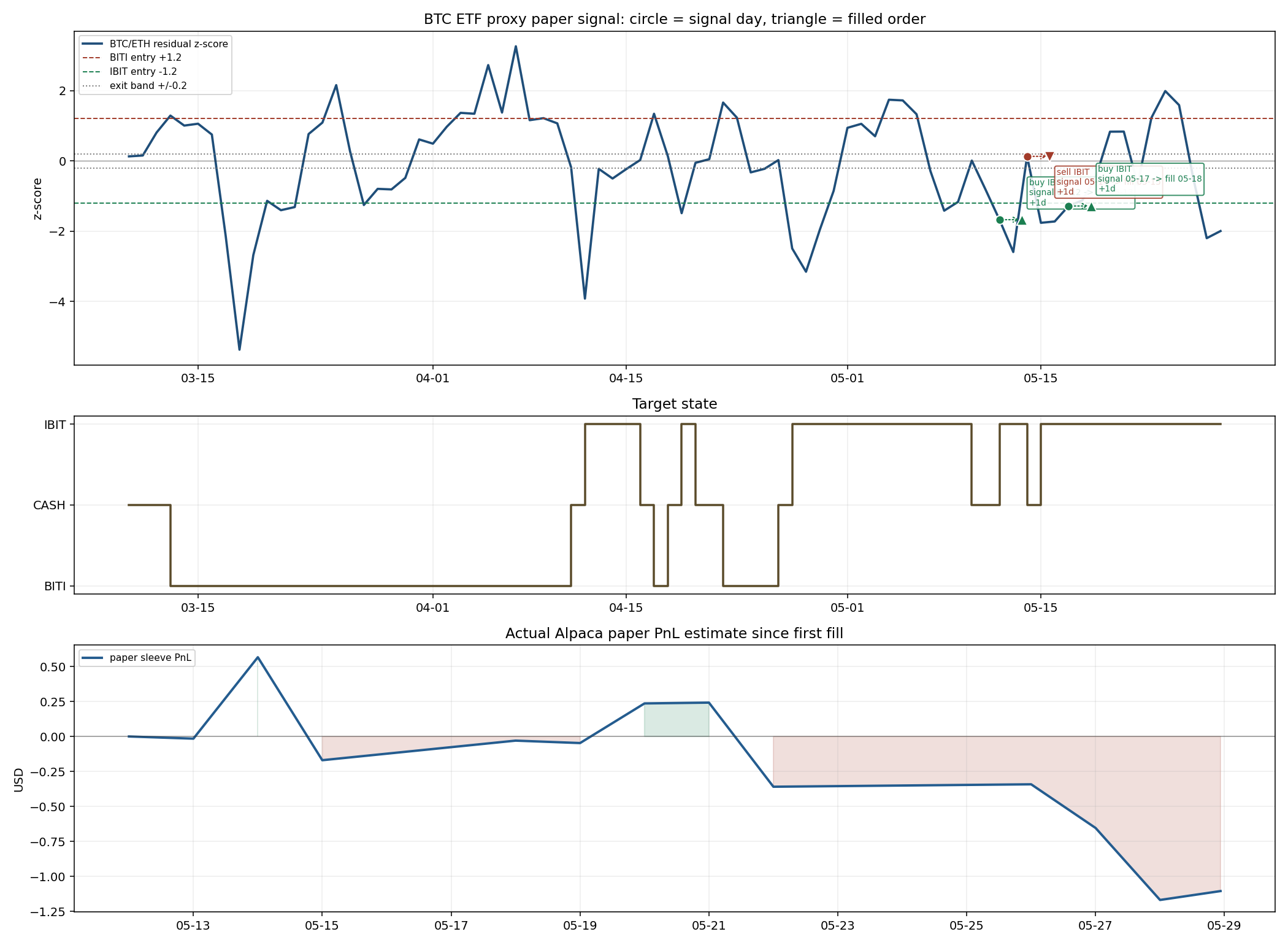

Current Paper Signal / Trades / PnL

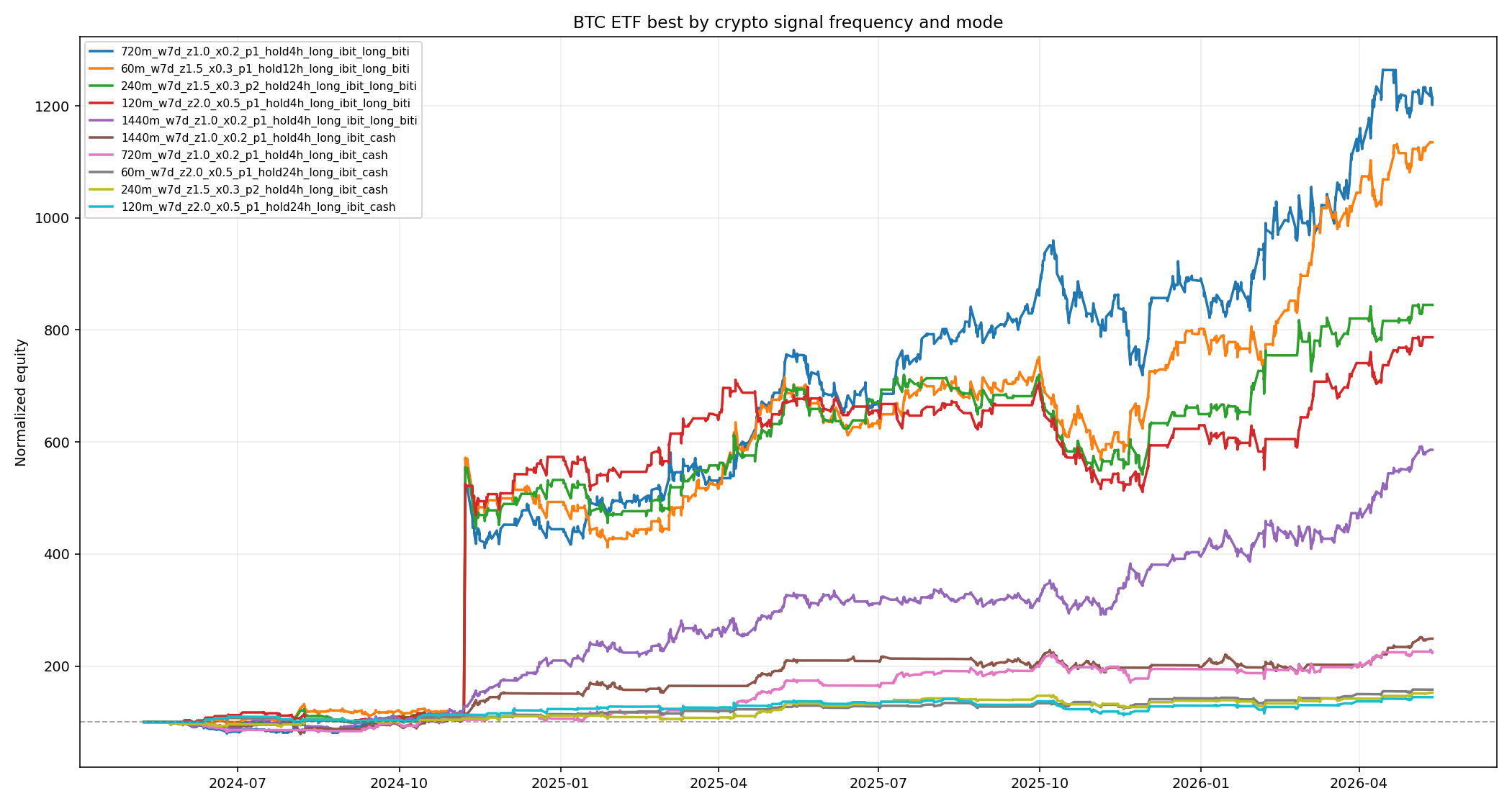

Intraday Frequency Research

Backtest Table

| Variant | Sharpe | Total Return | MaxDD | Trades / Year |

|---|---|---|---|---|

| BTC signal, long IBIT / long BITI | 1.8975 | 318.00% | -22.65% | 51.3 |

| BTC signal, long IBIT / short IBIT | 1.8089 | 287.18% | -22.71% | 51.3 |

| BTC signal, long IBIT / cash | 1.0505 | 78.53% | -29.45% | 26.9 |

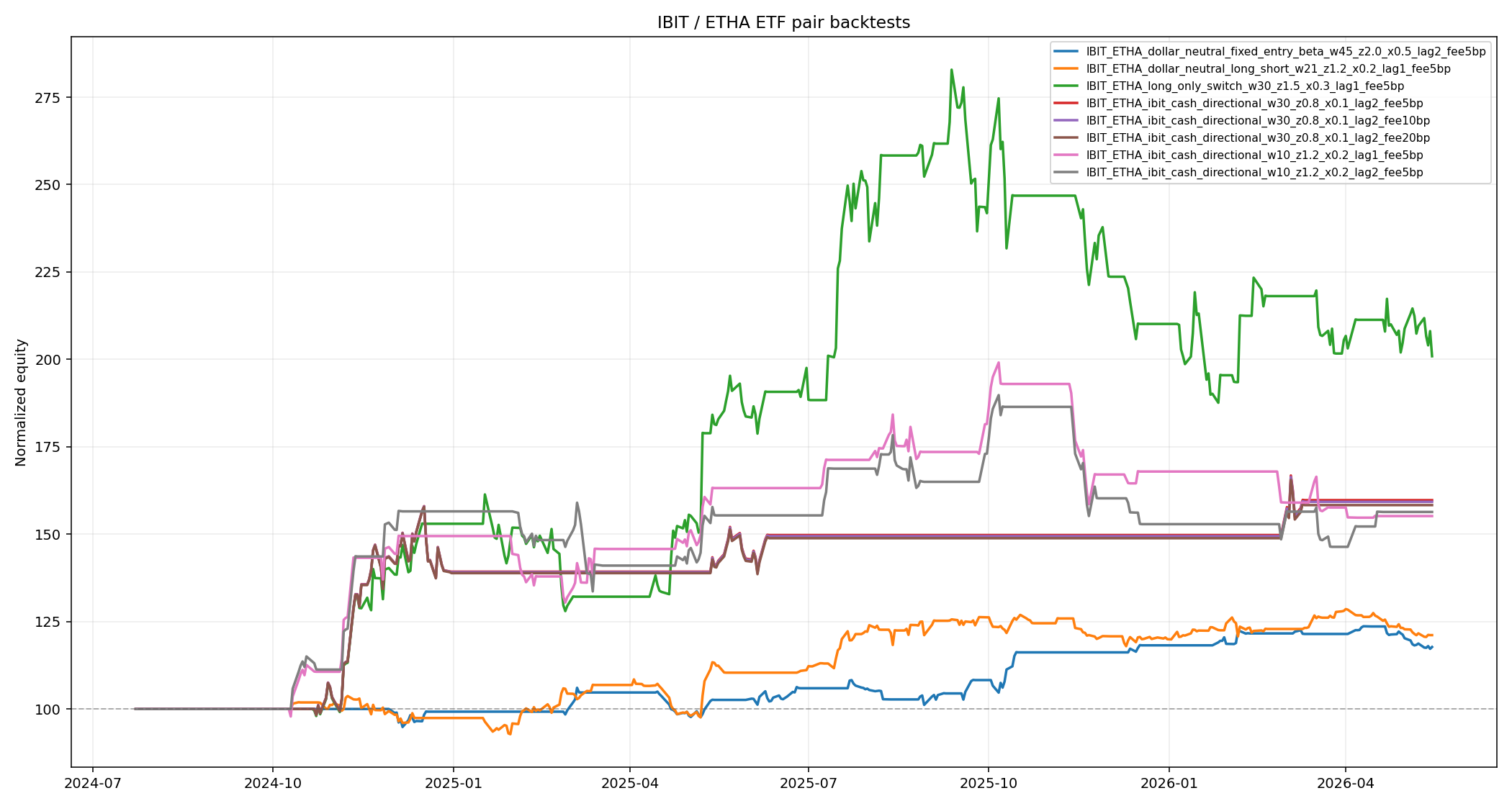

IBIT / ETHA Pair Extension

ETH ETF Pair Read

| Variant | Sharpe | Total Return | MaxDD | Trades / Year | Decision |

|---|---|---|---|---|---|

| IBIT/ETHA fixed-entry-beta pair | 0.9188 | 17.73% | -7.93% | 16.0 | Clean pair structure, useful as diversifier; not a replacement. |

| IBIT/ETHA daily-rebalanced pair | 0.7937 | 21.12% | -10.53% | 158.0 | Too much turnover for the achieved Sharpe. |

| IBIT/ETHA long-only switch | 1.1696 | 100.90% | -33.68% | 22.7 | Higher return, but drawdown is too large. |

Implementation Notes

Signal: rolling BTC/ETH beta, residual, and z-score are all lagged to avoid using future data. The live paper runner uses the prior completed crypto daily bar before trading US ETFs.

Execution: all paper orders go through AlphaVault Ops

ExecutionGateway. The runner checks market hours and

tradability, and only manages its own recorded IBIT/BITI quantity.

Review Links

| GitHub README | strategies/btc_etf_proxy_ibit_biti |

| Backtest artifacts | research_results/btc_etf_proxy |

| Backtest script | scripts/backtest_btc_etf_proxy.py |

| Paper runner | strategies/btc_etf_proxy_ibit_biti/paper_trader.py |